Business transfers, particularly of family businesses, are becoming increasingly common in Luxembourg. While the principle is well known, the mechanisms behind it are often less so and require anticipation work that is often underestimated.

What is meant by business transfer and what are the objectives?

The transfer of a business covers several scenarios. The entrepreneur may wish to retire or reduce his presence, while at the same time wishing to perpetuate his company, by transferring it to a third party buyer, a committed manager or a dynamic employee, or by ensuring a smooth family handover.

The transferor may also find himself obliged to reduce his shareholding to enable his company to be refinanced, or may wish to sell at the best price without worrying about the intentions of the acquirer.

Therefore, the transfer of a business, particularly a family business, has several objectives that go beyond speculative aspects: ensuring the survival and development of the company, avoiding family tensions linked to governance or the future sharing of profits, or retaining key employees.

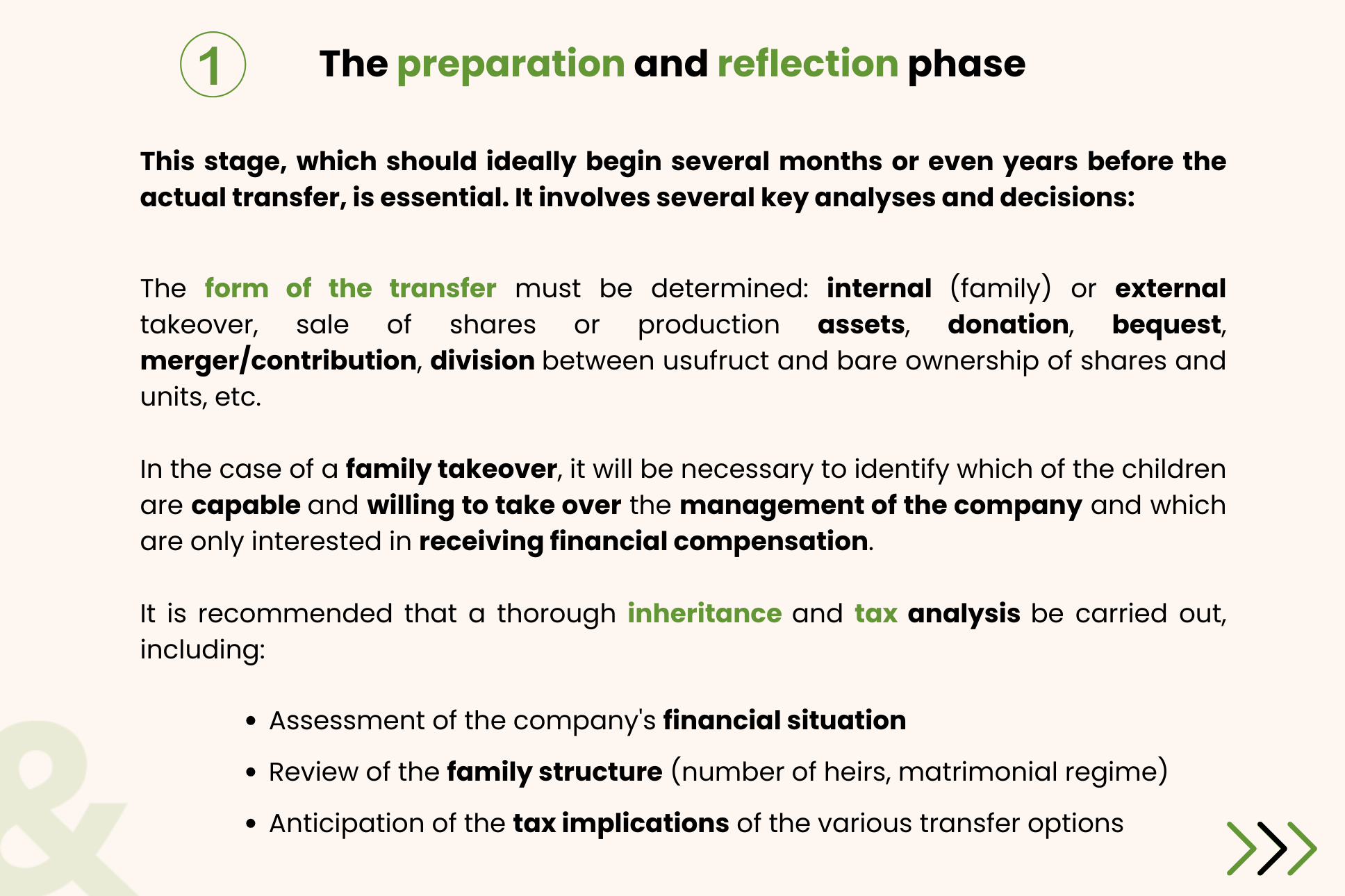

In order to take these specific objectives into account, it is important to prepare the necessary documentation (presentation brochure, key KPIs, data room, etc.) in advance, which will enable the parties to negotiate under the right conditions.

The prior tax study is often decisive in determining the ideal scenario for all parties

Foreseeing the transfer of a family business can be vital, especially when it does not take place in the direct line, or when it requires several companies to be brought together within a holding company before any transfer. In the case of gifts, donors may wish to retain the income linked to the shares transferred, in which case a split between usufruct and bare ownership could be envisaged. Anticipation is the key to success, while each situation will need to be analysed on a case-by-case basis in order to provide a tailor-made tax solution. In particular, capital gains on the sale of shares by an individual resident in Luxembourg may be exempt under certain conditions.

In all cases, complex structures that could be classified as aggressive tax planning should be avoided. European legislation has developed considerably in recent years (DAC, ATAD, etc.) and it is important to take this into account in any transaction with tax implications. If in doubt, a request for a tax ruling from the direct tax authorities may be necessary and is sometimes required in the sale/merger/contribution agreement.

Conclusion

The transfer of a business is a large-scale operation requiring the coordinated involvement of many legal and accounting specialists. Insufficient anticipation is likely to discourage buyers or even compromise the survival of the business, which will continue to operate during the transfer process.

Brucher Thieltgen & Partners can guide and advise you throughout the acquisition or transfer process and recommend specialists for the extra-legal aspects.

Do not hesitate to contact our experts:

Nicolas Bernardy: nicolas.bernardy@brucherlaw.lu

Sébastien Rimlinger: sebastien.rimlinger@brucherlaw.lu

Nicolas de Jonghe d’Ardoye: nicolas.dejonghe@brucherlaw.lu